If you own a residential property in Malta and rent it out, there’s one form you’ll hear about more than any other: TA24. It’s the mechanism through which most Maltese landlords settle their tax obligations on rental income — and it’s remarkably straightforward, provided you understand how it actually works.

The problem is that “straightforward” sometimes leads to assumptions. And the most expensive assumption a landlord can make with TA24 is thinking the rules work the same way as the standard income tax return. They don’t.

This guide focuses on private residential landlords and property managers using the Article 31D route — the most common approach for long-term lettings in Malta. It covers what the form is, where people go wrong, and what it means for your record-keeping.

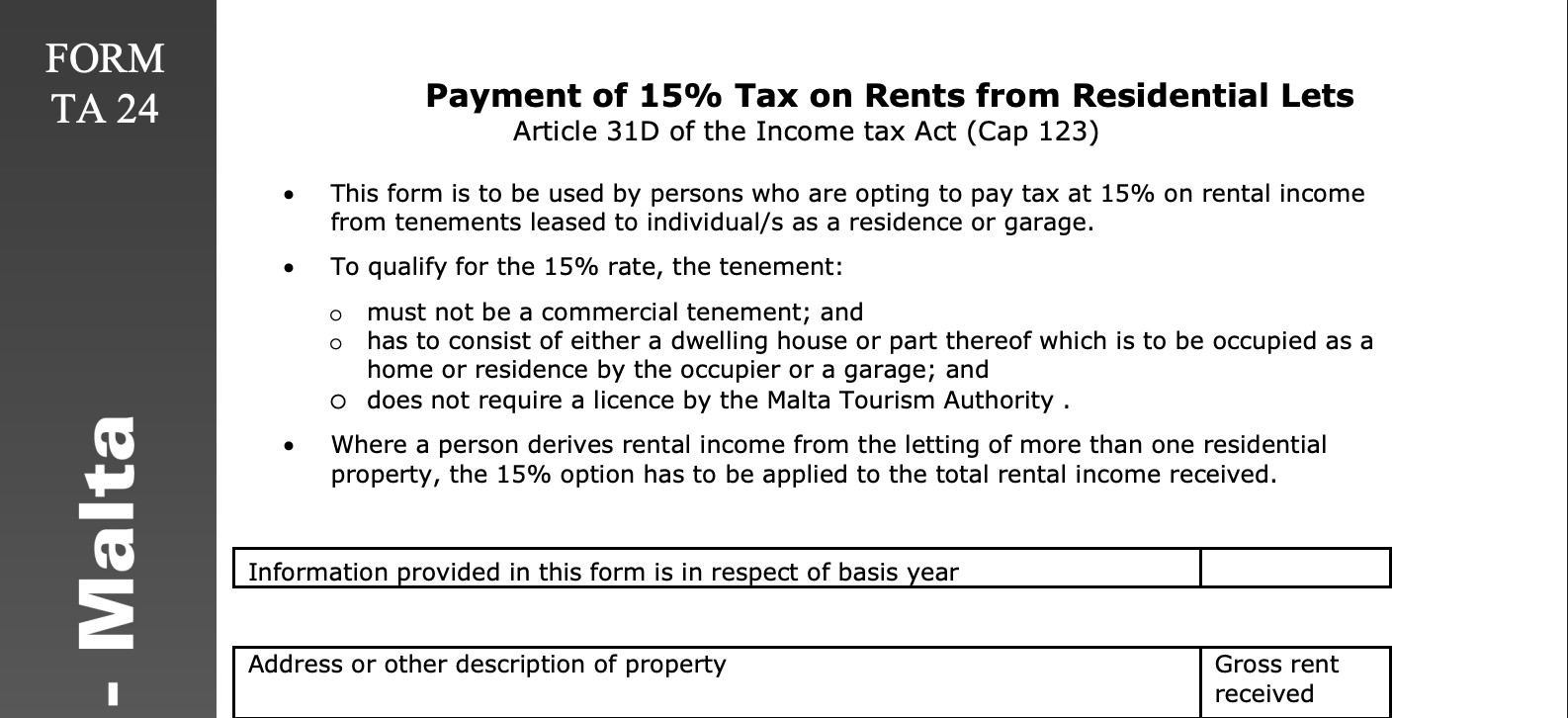

What is the TA24 Form?

TA24 is the prescribed form used to pay the 15% final withholding tax on rental income under Article 31D of Malta’s Income Tax Act. It covers both residential property (since 2014) and commercial property (since 2016). The regime is available to individual and corporate taxpayers, whether resident in Malta or not.

One important exclusion to be aware of: rent from related parties does not qualify. A body of persons is considered related to an individual if it is owned or controlled, directly or indirectly, by more than 25% by that individual. If your tenant is a company you control or a connected entity, the 15% route is not available.

The form, together with the tax payment, must be submitted by no later than the 30th of April of the year following the relevant rental year. For rental income received during 2025, the deadline is 30 April 2026.

Is the 15% Rate Compulsory?

No. Opting for the 15% final withholding tax is a choice, not a requirement. Landlords may alternatively declare rental income in their annual tax return and be taxed at applicable standard rates — progressive rates for individuals, the standard 35% corporate rate for companies.

For individuals, opting for the standard return also allows certain deductions: interest on property loans, ground rent paid, and a maintenance allowance. That can make the annual return route more attractive if your deductible expenses are substantial relative to income.

For most residential landlords, the 15% flat rate is simpler and often more tax-efficient. But the calculation is worth doing. If your total rental income is modest and your effective marginal rate would be lower than 15%, the deductions route may work out better. Discuss it with an accountant at least once.

If the 15% option is exercised, it applies to all qualifying rental income received in that year — you cannot split your portfolio, applying the flat rate to some properties and the annual return to others in the same tax year.

Individuals vs Companies: A Key Distinction

The TA24 regime is available to both individuals and companies, but the treatment differs in one important respect.

For individuals, if the 15% tax is paid via TA24, the rental income does not need to be declared in their personal income tax return. The TA24 fully discharges their tax obligation on that income.

For companies, the 15% is also a final tax, but the distributable profits resulting from such income — after the 15% has been paid — must be allocated to the Final Tax Account in line with Malta’s imputation system. Companies should ensure their accountant handles this allocation correctly; it’s not a manual step most landlords need to worry about, but for corporate property owners it matters.

The No-Deductions Trap

This is the most common misunderstanding among landlords new to the TA24 route — and the one that causes the most frustration.

Under the standard income tax return, landlords can claim deductions: interest on property loans, ground rent, and a maintenance allowance. It sounds appealing.

But under TA24, no deductions are permitted. Since the 15% is a final tax, it is calculated on your gross rental income — the full amount received from your tenant before any expenses. The official guidance is explicit on this point.

In practice, this means that if you spent €3,000 on repairs, boiler replacements, or management fees during the year, none of that reduces your TA24 liability. The 15% applies to everything you collected.

For many landlords this is still the better deal — the flat rate is predictable, administratively simple, and avoids the complexity of tracking deductible expenses year-round. But the calculation needs to be made consciously, not by assumption.

VAT: Generally Exempt for Residential Lettings

For standard long-term residential rentals, VAT is not something you charge to your tenants. Under the VAT Act, the letting of immovable property in Malta is generally exempt without credit from VAT. This means you do not charge VAT on rent, and you cannot reclaim VAT on related expenses such as repairs or furnishings.

There are, however, notable exceptions. Licensed tourist accommodation — villas, farmhouses, and similar — falls under a separate regime subject to VAT at 7%, plus eco-contribution obligations. Short-term lettings of 30 days or less can also be treated differently depending on the circumstances. Vehicle parking and certain commercial lettings to registered businesses are further carve-outs.

If your portfolio is purely long-term residential, the VAT exemption applies straightforwardly. But if any of your properties are let on short-term or tourist bases, the VAT treatment needs to be confirmed separately — it’s a different set of rules entirely.

The Housing Authority Rebate — A Bonus Worth Claiming

If your private residential lease is registered with the Housing Authority as a long private lease of 2 years or more, you may be eligible for a tax rebate that reduces your effective rate below 15%.

The rebate is available from basis year 2021 onward, applies where tax on the lease is being paid at the rate of 15%, and is claimed through the online TA24 filing. The rebate for any year cannot exceed 15% of the rent derived for that same year — meaning in the most favourable cases it can reduce the net tax to zero on that particular lease.

The amount of the rebate depends on the duration of the lease and the number of bedrooms in the property. The specific bands are set by the Commissioner for Revenue and are available through the online TA24 form; your accountant will be able to confirm the applicable figures for your lease.

For very long-term arrangements, there is an additional incentive: property rented to the same tenant for more than 7 years under a Housing Authority scheme may benefit from a reduced rate of just 5% final withholding tax under Article 31E.

If your leases are registered and meet the qualifying conditions, make sure the rebate is being claimed. It won’t be applied automatically — it needs to be included in your TA24 submission.

What Happens if You Don’t File?

Failing to declare rental income is not a grey area. Where rental income has not been declared, the taxpayer is exposed to higher tax, interest, and penalties.

The exact consequences depend on whether the lessor is an individual or a company. For companies, the applicable rate on undeclared rental income following investigation is 35% of gross income. For individuals, undeclared income may be taxed at progressive rates rather than the flat 15%, in addition to interest and additional tax under the Income Tax Acts. In all cases, the ability to benefit from the 15% final withholding tax regime is lost.

A cleaner way to think about it: if you do not declare rental income, you may lose the ability to benefit from the 15% flat rate and become exposed to materially higher tax, interest, and penalties. This is an area where professional advice is worth getting before any issue arises, not after.

Filing on time — even if some numbers need to be refined — is always preferable to a late or missed submission.

TA24 and Property Management: Getting the Numbers Right

The TA24 calculation itself is simple: 15% of gross rental income received during the calendar year. But assembling that number accurately — especially if you manage multiple properties, deal with partial-year tenancies, or have any arrears — requires organised records.

This is where property management software earns its place. If you’re using Apartemo to track rent collection, you have a clear, itemised record of every payment received across your portfolio, broken down by property and by month. When April approaches and the TA24 deadline arrives, the gross income figures are already there — no spreadsheet archaeology required.

For letting agents and managers preparing the TA24 on behalf of landlords, the same logic applies. The agent needs accurate gross income figures per property per year. Clean records mean a faster process and less risk of a figure being missed or estimated incorrectly.

Apartemo’s financial reporting gives landlords and managers a real-time view of rental income across their portfolio, with filtering by property, date range, and tenancy. It doesn’t replace your accountant — but it means you’re never starting the tax season from scratch.

Quick Summary

- TA24 is used to pay the 15% final withholding tax on gross rental income in Malta, under Article 31D

- The deadline is 30 April of the year following the rental year

- The 15% is optional — landlords may instead declare via their annual return and claim deductions

- The 15% applies to gross income — no deductions are allowed under this route

- The regime applies to all qualifying rental income in a given year; you cannot split properties between methods

- Rent from related parties does not qualify for the 15% regime

- Residential lettings are generally VAT-exempt; tourist and short-term accommodation is not

- Long private leases of 2+ years registered with the Housing Authority may qualify for a tax rebate — claim it through your TA24

- Non-declaration exposes landlords to higher tax, interest, and penalties; the 15% flat rate is lost

- Individuals and companies are treated somewhat differently — companies need to allocate profits to the Final Tax Account

This article is for informational purposes only and does not constitute tax or legal advice. Regulations and rates are subject to change. Consult a qualified Maltese accountant or tax adviser for guidance specific to your situation.

Ready to transform your property management?

Join hundreds of property managers who trust Apartemo to streamline their operations.

Start Free Trial